Materials, labor, production supplies, and factory overhead are all included in these prices. Both strategies require careful planning and execution, but the rewards can be significant. By improving product quality, manufacturers can reduce material costs while reducing warranty expenses and increasing customer satisfaction. Reducing waste helps companies save on both the cost of raw materials and disposal fees.

How to Identify and Classify Direct Expenses

Alternatively, there are indirect material expenses – they all contribute to the workers being able to do their job well. Process costing is used to calculate the cost of producing a large number of identical products. know the facts about the fair tax This method is typically used in manufacturing environments where products are made in large batches. The total cost of production is divided by the number of units produced to arrive at the cost per unit.

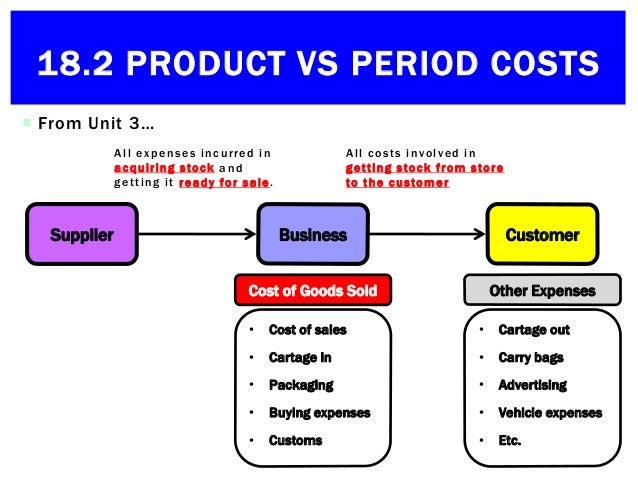

Product costs and period costs

In summary, the difference between product costs and period costs is that product costs are directly tied to the production of a specific product. In contrast, period costs are not directly connected to the production of a particular product and are expensed in the period in which they are incurred. However, undercosting can also be a sign of inexperience or poor planning. Business owners who do not have a clear understanding of their costs are more likely to underprice their products or services. This can lead to financial problems down the road, as the business may not be able to cover its costs and become profitable. With a bit of time and effort, businesses can be well on their way to managing products more efficiently and profitably.

Please select the country and language to view the products tailored for your location.

Product cost accounting is crucial for gaining insights into the profitability of a business. It helps you understand the financial implications of your decisions and accurately assess how much it costs to produce a given product. This purchases budget is required to calculate the amount of raw material that needs to be purchased for the production process and estimate the related costs. However, it is always better to calculate this cost per unit as it can help decide the appropriate sales price of the finished product.

Understanding the Costs in Product Costs

Everything that happens during a month and involves money has to be taken into account. Otherwise, you won’t know where the money went and how to avoid it in the future. Integrate financial data from all your sales channels in your accounting to have always accurate records ready for reporting, analysis, and taxation.

The maintenance of precise financial records demands the identification as well as desegregation of direct expenses. Following a definite process with these costs helps ensure they are accounted for and captured in the COGS. Below is an elaborate procedure for identifying and classifying direct expenses.

By investing in robust product costing practices, businesses position themselves for success and create a strong foundation for long-term prosperity. Direct materials are the raw materials directly involved in the production process. For instance, in a manufacturing facility producing furniture, the wood used would be considered a direct material. Product cost also plays a pivotal role in the preparation of financial statements. It forms a significant part of the ‘Cost of Goods Sold’ (COGS) on the income statement, directly affecting the company’s gross profit and net income. A lower cost of production can lead to a higher gross profit margin, assuming the sales price remains constant.

Understanding these types of production costs is crucial for accurate cost accounting and effective management of production costs. To better understand how product costing works, let’s apply the formulas above to a real-life example. Product cost management requires careful consideration of materials, labor, overhead expenses, research & development costs, marketing costs, and more. If you are thinking of undercosting your products or services, weighing the risks and potential consequences is important.

Managing product and production costs is essential for a successful business operation. It’s crucial to develop strategies to reduce production costs while controlling product costs so prices remain competitive. With careful planning and analysis, businesses can effectively manage product and production costs to maximize profitability. On the other hand, if production costs decrease due to increased efficiency or automation, then this could lead to lower product costs. These costs consist of direct labor, direct materials, consumable production supplies, and factory overhead expenses.

- Direct expenses are often considered variable as it changes with the level of activity or output.

- She holds a Masters Degree in Professional Accounting from the University of New South Wales.

- Since product costs include manufacturing overhead that is required by both GAAP and IFRS, product costs should appear on financial statements.

- If you divide your overall costs among different accounts and analyze the same accounts each month, you’ll see which of these costs are not essential, irrational, or growing.

- If a particular product makes profit, it can make sense based upon its profitability.

But for a production cost to get labeled as an expense, it must get incurred when producing the product or service. Production might include things like rent, direct labor costs, raw materials, and machinery. Manufacturing overhead includes all the costs related to the production process that are not direct materials or direct labor. These costs are incurred in the manufacturing facility and are necessary for production but cannot be directly linked to specific units.